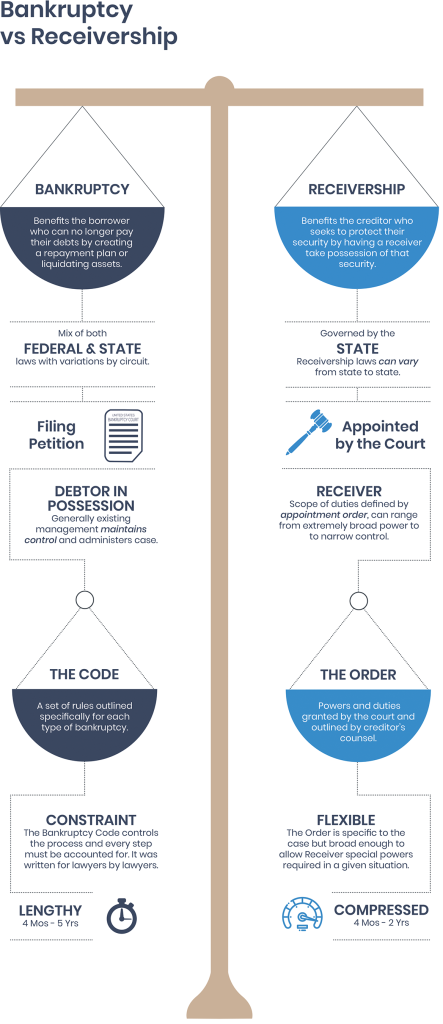

When borrowers and creditors reach a standstill in default payment remedies, borrowers may have the option to seek protection in the Bankruptcy Courts for resolution to their financial situation.On the other hand, receiverships are a viable solution for creditors looking to maximize value that can be cheaper and more expedient than a bankruptcy proceeding. Both options play an important part in distressed businesses.

Receiverships are governed by the Order of Appointment. The order sets forth the custodial responsibility of the receiver over the receivership estate. The order is flexible, specific to the case, and broad enough to allow the receiver special or unusual powers that the receiver may require in a given situation. The judge who issues the order can define virtually any procedures, rules, mechanisms, etc. that the court deem appropriate under the circumstances. This allows the receivership to be tailored to the circumstances of the case to a much finer degree than a bankruptcy.

Chapter 11 is given structure by the Bankruptcy Code and the Rules of Bankruptcy Procedure. The bankruptcy proceeding is a defined and intentional process. It is a very formal legal procedure set forth for dealing with financial and other issues that allows for a resolution based on an equitable outcome. In a receivership, the resolution can be a disproportionate outcome brought on by the receiver for the benefit of the receivership estate, whereas the outcome in a bankruptcy filing is impartial and is a function of the bankruptcy plan.

The Proceedings

In financial situations where the business or operational problem lies in management, a receiver may be a more effective approach for creditors and investors. In financial situations where money is the business problem, bankruptcy may be a good course of action.

Below are additional scenarios to consider when determining the appropriate course of action for debt solution.

Continued Business Operations

Receivership

Has the advantage to facilitate the continued operation of a business or the rehabilitation of an enterprise before sale to a third party.

Chapter 11

The prime consideration is to reorganize the company to allow for continued operations.

Replacing Management

Receivership

Has unilateral control and can make managerial decisions, however big or small, for the receivership estate within the authority granted by the receivership order.

Chapter 11

Management typically remains in control of the company with a stated goal of restructuring the company, both financially and operationally.

Assume or Reject Existing Contracts

Receivership

Has the power to enter into, terminate, and negotiate contracts and service agreements for the benefit of the estate.

Chapter 11

Allows for the acceptance or rejection (and potential renegotiation of contracts) subject to certain conditions being met.

Infusion of Capital

Receivership

Additional capital can be invested with confidence that it will be applied for the sole purpose that it was requested without influence.

Chapter 11

Debtor-in-possession financing allows the enterprise to have access to additional capital to address operational needs.

Pursue Litigation

Receivership

The receiver has the authority to issue demands and institute, continue, or otherwise address all legal actions on behalf of the estate to preserve and recover all amounts that may be due.

Chapter 11

The receiver has the authority to issue demands and institute, continue, or otherwise address all legal actions on behalf of the estate to preserve and recover all amounts that may be due.

Conclusion

What makes most sense for a business in a financially distressed situation – a Chapter 11 filing or a receivership? The short answer is that it all depends on the situation. In a Chapter 11 filing, the goal is to restructure the business while simultaneously attempting to satisfy the needs of parties that have an economic interest in the estate. In a receivership, the goal is to maximize returns of the assets typically to one or more creditors. Though the circumstance that prompt these two options may be similar, the approach can be materially different. The outcome, on the other hand, can be one of many things; reorganization, turnaround, sale of entity, or liquidation. A Chapter 11 and a receivership are solutions that are extremely important to a company in financial distress. It is important to understand each solution to better steer the enterprise in the right direction for debt solution.